Sustainability Reporting After the Omnibus: Less Obligation, More Conviction

- Felipe Gärtner J

- Apr 7

- 3 min read

The European Commission's Omnibus simplification package¹ has reshaped the sustainability reporting landscape significantly. By narrowing the scope of the Corporate Sustainability Reporting Directive (CSRD), it reduced the number of companies subject to mandatory reporting from roughly 50,000 to 10,000 — an 80% contraction.² Some experts interpreted this as a blow to the ESG consulting and software market. On paper, they are not wrong.

But that reading misses what is actually happening on the ground.

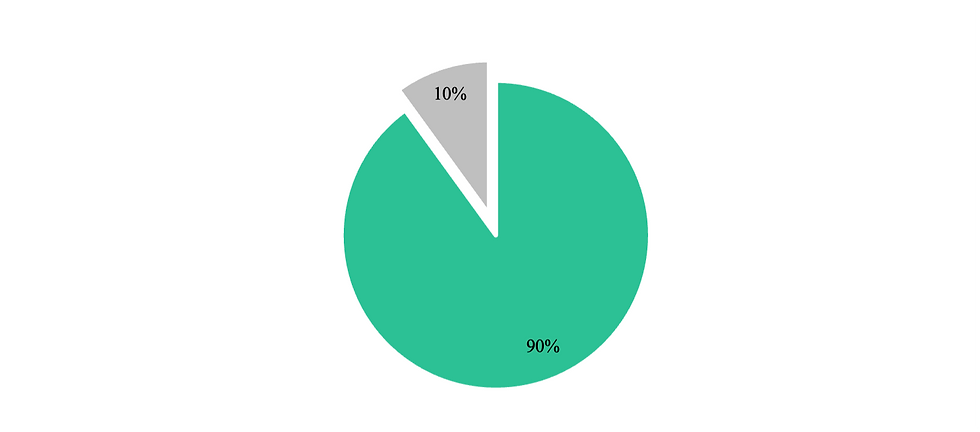

A recent Osapiens survey of 403 large European firms found that 90% of companies removed from the CSRD scope still plan to continue or expand their sustainability reporting voluntarily.³ The same share has already integrated sustainability disclosures with their financial reports, and 88.9% expect to increase investment in reporting technology and automation within the next year. Across the Atlantic, the U.S. Securities and Exchange Commission has similarly stepped back from its climate reporting rule — yet corporate behavior is not following regulators toward the exit.

Graph 1. Companies planning to expand or continue sustainability reporting

Source: Osapiens Survey

The reason is straightforward: sustainability data has outgrown compliance. It now drives decision-making across operations, supply chain risk management, innovation pipelines, and capital allocation. As Osapiens concludes, sustainability disclosure is no longer a regulatory checkbox — it has become a core element of corporate governance and risk management.

This does not mean the transition is frictionless. The Sustainability Transformation Monitor published by the University of Hamburg shows that sustainability momentum is under pressure — not because executives have deprioritized it, but because political uncertainty and weak market incentives are creating hesitation at the implementation level.⁴ Even so, in 73% of companies surveyed, accountability for sustainability transformation remains anchored at the board or senior management level.

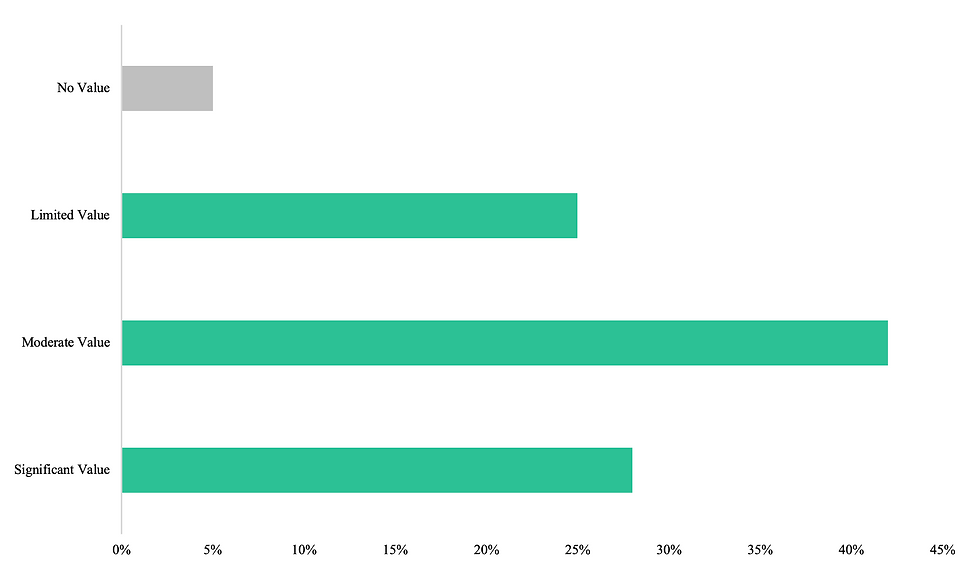

The reason leadership stays engaged is that sustainability data has proven its commercial case. PwC's Global Sustainability Reporting Survey found that 95% of companies report deriving some value from sustainability data beyond compliance — 28% describe that value as significant, and a further 43% as moderate. Part of that return comes from an often-overlooked organizational effect: gathering the data required for sustainability reporting forces cross-functional dialogue between teams that rarely interact otherwise, surfacing synergies, inefficiencies, and cost reduction opportunities that would otherwise remain invisible. Thirty-eight percent of companies already use sustainability data extensively for business strategy. The companies capturing the most value are also investing the most: among those reporting significant returns, 56% substantially increased resources dedicated to sustainability reporting over the past year, and 40% increased senior leadership time — compared to just 26% and 16%, respectively, across all respondents. The commitment is structural, even when the path forward is unclear.

Graph 2. Value obtained from data and insights from CSRD/ISSB reporting

Source: PwC Ireland

This is precisely the environment where tools like Caribou become most valuable. When reporting shifts from mandatory to voluntary, the obligation is replaced by judgment — and judgment requires better data. Caribou's dashboards, intuitive interface, and streamlined reporting capabilities give decision-makers the clarity to understand their operational risks and supply chain exposures, stay ahead of evolving regulatory frameworks, and embed sustainability into the strategic core of the business rather than treating it as a peripheral compliance exercise.

Less regulation does not mean less reporting. It means reporting that is driven by conviction rather than obligation — and that is a more durable foundation to build on.

Bertelsmann Stiftung, Stiftung Mercator, University of Hamburg, & Peer School for Sustainable Development.(2026, February 26). Sustainability Transformation Monitor 2026: Sustainability remains a top priority in companies—But the momentum is gone. University of Hamburg. https://www.uni-hamburg.de/en/newsroom/presse/2026/pm5.html

Council of the European Union. (2026, February 24). Council signs off simplification of sustainability reporting and due diligence requirements to boost EU competitiveness [Press release]. https://www.consilium.europa.eu/en/press/press-releases/2026/02/24/council-signs-off-simplification-of-sustainability-reporting-and-due-diligence-requirements-to-boost-eu-competitiveness/

Responsible Investor. (2026, March 2). ESG round-up: Majority of German firms no longer in CSRD scope plan voluntary disclosures. https://www.responsible-investor.com/esg-round-up-majority-of-german-firms-no-longer-in-csrd-scope-plan-voluntary-disclosures/

ESG News. (2026, March 11). Osapiens survey: 90% of European companies continue sustainability reporting after EU omnibus changes. https://esgnews.com/osapiens-survey-90-of-european-companies-continue-sustainability-reporting-after-eu-omnibus-changes/

PwC Ireland. (2026, March 16). PwC’s Global Sustainability Reporting Survey 2025: Sustainability reporting at a turning point—Lessons from early adopters. https://www.pwc.ie/reports/sustainability-reporting-survey.html

Mohin, T. (2026, March 20). Sustainability reporting isn’t going away. Sustainability Simplified. https://www.sustainabilitysimplified.eco/p/sustainability-reporting-isn-t-going-away

Comments